FPH regularly conducts materiality assessments to identify priority non financial ESG indicators. These indicators inform the Company’s ESG program and set how the Company monitors ESG progress.

The list of material ESG topics are reassessed every two to three years by an independent third party. The FPH ESG material topics were last reassessed in 2022 using a double materiality approach, and is set to be reviewed in 2025. The methodology to assess the material topics are discussed further in this section.

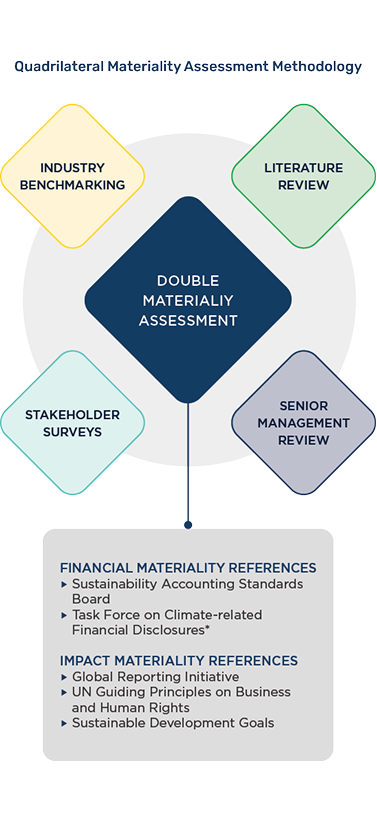

Quadrilateral Assessment and Double Materiality

FPH commissioned the University of Asia & Pacific – Center for Social Responsibility (UA&P–CSR) to assess its ESG material topics.

The Quadrilateral Materiality Assessment Tool was developed by UA&P — CSR to capture “true impact reporting” and the Double Materiality Approach. The Double Materiality Approach melds financial and impact materiality to emphasize how the company creates economic value for its investors while also contributing to sustainable development.

Pertinent ESG topics were surfaced through a four-pronged procedure involving literature review, peer benchmarking, senior management consultations, and stakeholder consultations. After the process of surfacing ESG topics, prioritization is conducted with further discussions with the Corporate Sustainability Group and FPH Senior Management.

The methodology ensures that the ESG topics assessed are grounded on current standards and best practices; local policies such as the ESG reporting requirement of the Philippine Securities and Exchange Commission (SEC); and international commitments. The report adopted corresponding standards and frameworks for multiple stakeholders at FPH. These standards considered the perspectives of internal and external stakeholders such as customers, employees, vendors and partners, government, communities, and investors.

*IFRS-S2 is broadly consistent with TCFD

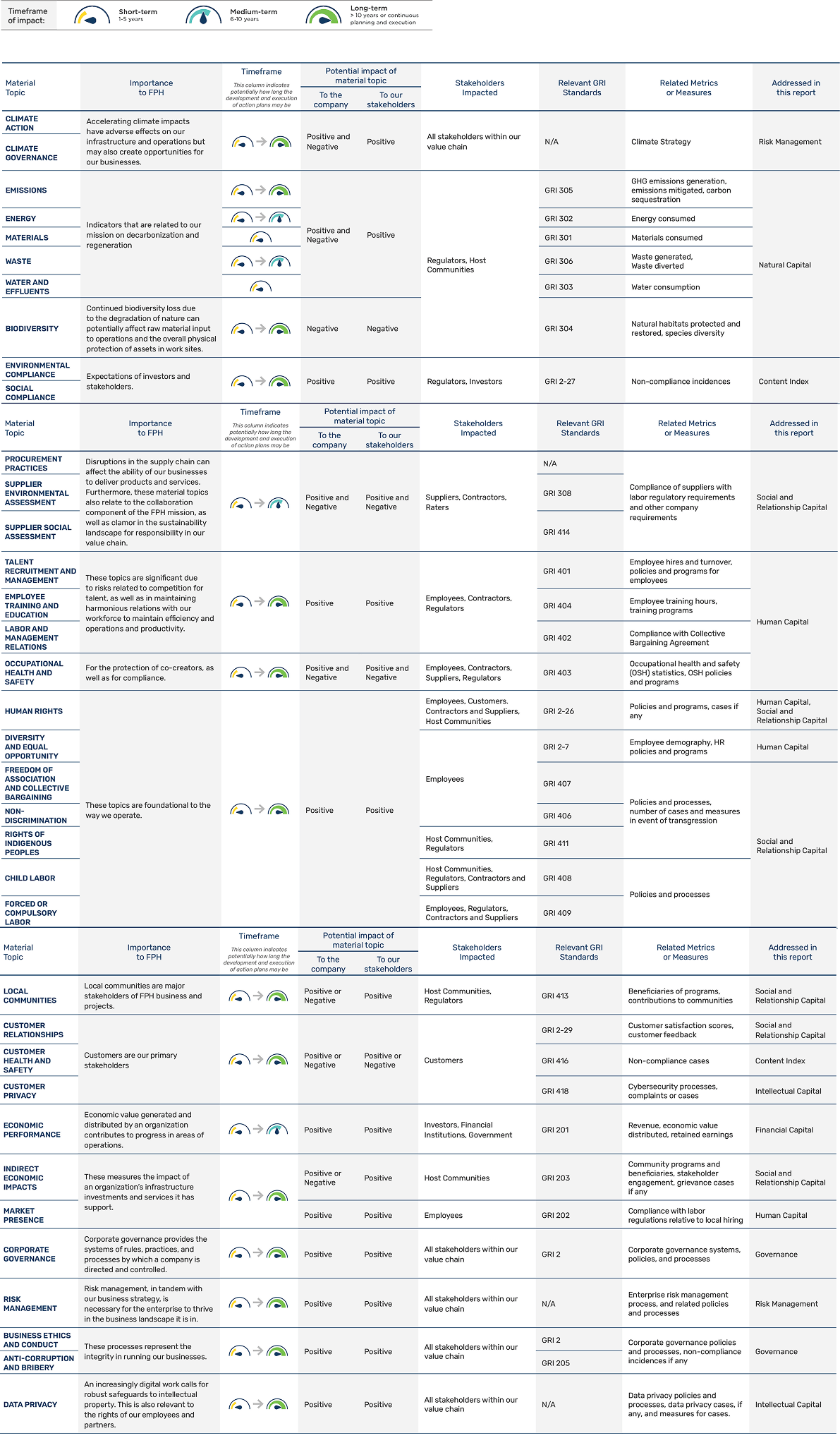

Materials Topics

The materiality assessment of 2022 resulted in 37 material topics. After considering changes in the business environment and a review of other internal and external factors, the list of the material topics was amended to 36. The changes made were as follows:

► The COVID-19 pandemic was no longer seen as a threat and dropped from the list; and

►The time frame of the impact for 3 classes of material issues (procurement related, talent-related and corporate governance-related) were amended from medium-term to short-term.